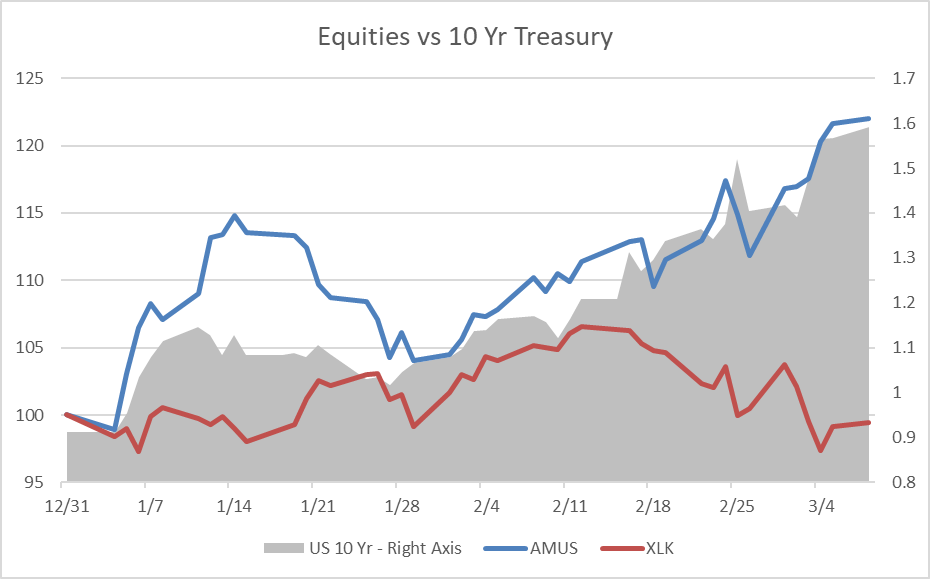

Are you worried about inflation? This has been an increasing market focus in recent weeks with the likely passage of the $1.9 trillion-dollar Covid relief bill (on top of all the other fiscal and monetary stimulus already in effect), ongoing wide-scale vaccine deployment, commodity prices moving higher than many expected—and possibly more alarming, the sudden rise in interest rates. While absolute rates are still very low, the pace of the increase in the 10-year Treasury yield caused market jitters and corresponded with a selloff in higher valuation multiple, longer-duration cash flow stocks, such as Clean Energy and Tech. In the chart below, we compare the Midstream Energy group (AMUS: Alerian US Midstream Energy Index) to the market darling XLK ETF (Technology Select Sector SPDR Fund) to illustrate the diverging performance trend.

Source: Bloomberg

For several months now, we have advocated increasing exposure to the Midstream space for a host of reasons (see our most recent webcast here). More specifically, though, we believe this group will continue to outperform as the re-opening/cyclical trade unfolds—and while there are no performance guarantees with an interest rate shock, this group has built-in advantages in an inflationary environment:

- Current Income with Growth: The average yield for the Midstream group remains high, approximately 8%, with projected dividend growth of ~2% over the next several years1. Additionally, as Free Cash Flow after dividends is positive and expected to increase, several management teams have stated they can supplement modest dividend growth with potential share buybacks.

- Yield Spread: With valuation multiples for the group still below pre-Covid levels and a yield spread of a historically high ~600 basis points, we believe there is plenty of “buffer” for the group to absorb an increase in the 10-year Treasury yield.

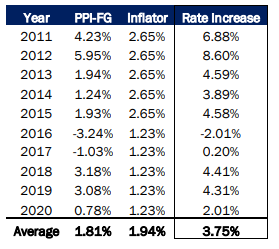

- Contract Protection: Many Midstream contracts have inflation escalators. For example, FERC regulated interstate liquids pipelines can increase tariffs by a percentage equal to the change in the producer price index for finished goods (“PPI-FG”) plus 0.78%. The below table shows what has generally been a nicely positive revenue driver well in excess of inflation.

Source: East Daley, “FERC Throws Liquids Pipelines a Bone”, January 5, 2021 - The Dollar: A weakening dollar is supportive for crude prices (denominated in US dollars), all else equal, and this can promote drilling activity and higher throughput for midstream systems—or, at the very least, higher commodity prices can fuel positive investor sentiment for the broader Energy group, which has been the case in recent months. And speaking of inflation, we thought it was worth pointing out that, nearly 1 year later, we’ve had a roughly $100/bbl increase in WTI crude since that historic bottom (-$37.63 on 4/20/20). Further, with propane prices up nearly 30% this year, and natural gas prices potentially moving materially higher after Storm Uri devastated Texas and depleted gas storage, the deflationary energy input trend that has persisted for so long is set to reverse.

- Energy Demand: Not all increases in interest rates are bad. When driven by economic growth (which typically corresponds to better energy demand), rising rates are generally seen as a positive. In their 2021 outlook, Kinder Morgan management expects gasoline and diesel volumes to be on average only 2% below 2019 levels for the year, with jet fuel volumes 12% below 2019 for the year. All products, however, are expected to trend higher and reach/approach 2019 levels by the fourth quarter of this year.

- Cyclical Trade and Momentum: The shift to cyclicals (Energy included) is clearly in full effect. Further, with outperformance for the Energy group over the past several months, there is an increasing likelihood that “momentum” trading baskets will be rebalancing to a net-long Energy position, which would obviously be a nice positive.

If you want to discuss any of these issues further, or how an allocation to Midstream could better position your portfolio for rising inflation, feel free to reach out to our team.

Notes:

1Wells Fargo Securities LLC Equity Research, “Comparative Valuation Tables”, 3/5/2021.

Disclaimer:

The information provided does not constitute investment advice and is not an offering of or a solicitation to buy or sell any security, product, service or fund, including any fund that may be advertised.

All information provided herein is for informational purposes only and should not be relied upon to make an investment decision.

Any charts, tables, and graphs contained in this document are not intended to be used to assist the reader in determining which securities to buy or sell or when to buy or sell securities. Any projections or other information in this blog post regarding the likelihood of various future outcomes are hypothetical in nature and do not guarantee any particular future results. Additional information is available upon request. Unless otherwise noted, the source of information for any charts, graphs, and other materials contained here is BPCFA.

This document may contain forward-looking statements and projections that are based on our current beliefs and assumptions and on information currently available that we believe to be reasonable; however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements.