Portfolio Manager Ben Cook, CFA, shares his insights on the current state of the energy market, discusses valuations and yields for midstream companies, and details the factors that set these companies apart.

Would you summarize the current state of demand for energy and commodity prices?

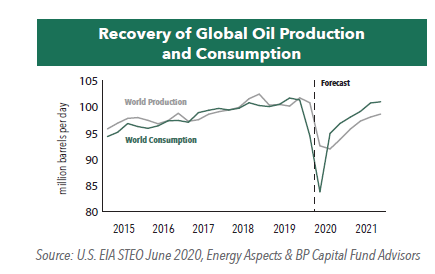

Following the demand destruction for oil due to the COVID pandemic, we have begun to see rising demand associated with the revival in economic activity as global economies reopen. Following extreme commodity price volatility in the first part of the year, by mid-June crude oil prices had strengthened, rising into the high $30s per barrel (NYMEX WTI).

We anticipate that the price of crude oil will remain in the high $30s for the remainder of 2020 and should be in the $40s in 2021. In this range, many U.S. energy companies can bring curtailed production back online. We see strong signs of demand recovery underway, and barring a second wave that causes subsequent lockdowns, we expect to return to pre-COVID demand levels in the second half of 2021.

In contrast to the collapse in demand for crude oil, U.S. natural gas demand in 2020 is estimated to decline by only 3-4%, and the long-term fundamental growth trajectory for natural gas remains largely unchanged. On the supply side, natural gas production associated with crude oil volumes will likely decline given the reduction in oil directed drilling, which should provide support for natural gas prices through year end 2020 and into 2021.

How have midstream companies reacted?

Despite the challenges faced by the broader Energy sector year to date, midstream companies have demonstrated remarkable resiliency. Companies quickly reduced their capital spending, and as a group capital expenditure budgets have been cut by approximately 40% on a year on year basis. Where possible, some midstream companies have redirected activity to focus on business lines that remain relatively strong, such as storage and energy export. Across the midstream sub-sector, we see little change in forecasted operating and financial results. The median change in 2020 EBITDA guidance has been lowered by only 6% versus pre-COVID levels, and companies are projecting a recovery in EBITDA in 2021.

How do current valuations look for midstream energy companies?

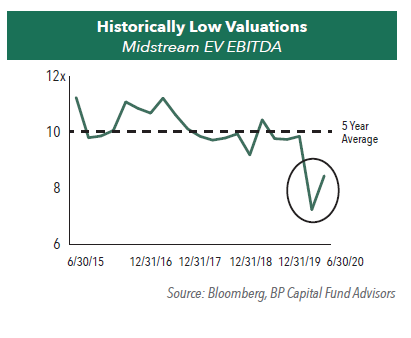

Midstream stocks tend to overshoot to both the upside and downside, and we certainly experienced the downside extreme in March. In fact, the stock prices of many of the companies we follow were impacted by aggressive selling by closed-end midstream funds which were forced to liquidate holdings in order to comply with fund leverage mandates. This type of selling tends to be price-insensitive, which typically results in wide price swings. While much, if not all, of this selling pressure has since passed, the sector remains at a significant discount to its historical average valuation level.

Given the unique structure of midstream MLPs and C-Corps, the valuation metric commonly used to evaluate midstream companies and compare to other sectors is Enterprise Value to EBITDA. As a group, midstream companies are trading at 8.5x EV/EBITDA, near the lows seen during the Great Financial Crisis. Current multiples are approximately 15% lower than at the beginning of 2020 and versus their five-year average, and well below the 10.5x at the end of the oil price collapse in 2016, despite these companies being in a much stronger financial position today than they were then.

Importantly, we do not believe that current equity prices yet reflect the improving fundamental supply/demand forecasts.

How are midstream companies better positioned now than they were during prior cycles?

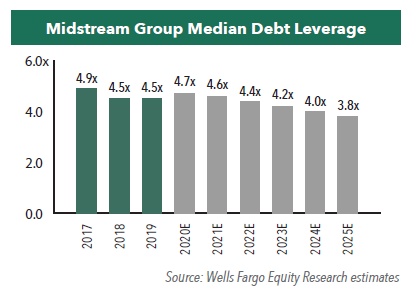

We are optimistic about the midstream space because of the broader structural changes that have occurred over the last few years. Midstream management teams have become better allocators of capital, placing greater focus on leverage reduction and free cash generation.

Corporate governance has also improved, as few of the midstream companies in the sub-sector remain encumbered by onerous management compensation incentives, and many of the companies we follow have moved to a more defensive cash payout coverage level, opting to retain significant amount of cash over and above that which is distributed to investors. In our view, this favorable trend speaks to the good visibility of future company cash payouts.

Midstream companies have also become more self-reliant for funding, and less dependent on capital markets, which decreases the likelihood of new equity issuance that potentially dilutes shareholders’ earnings per share.

What is the current yield on midstream stocks, and where do you see payouts going from here?

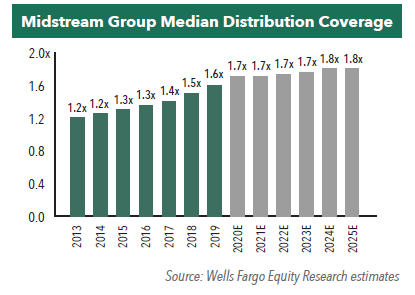

Currently at over 9%, yields on midstream companies as a group are very attractive. Distribution coverage is relatively high at 1.7x and is forecast to grow, making payouts more sustainable than, we believe, they have ever been.

Aggregate cash payouts from midstream companies in 2020 will likely be lower than they were in 2019, however, we believe midstream companies are exceptionally well positioned to weather the current environment, and payout cuts appear to now be behind us.

Going forward, we believe midstream companies have the financial strength to resume growing their payouts in 2021 and beyond.

What should investors look for among midstream energy companies?

The combination of historically attractive valuations, relatively high yields coupled with the prospect for rising payouts, and continued improvement in fundamentals make now an opportune time to consider an investment in midstream energy companies. However, deep understanding of the nuances of midstream MLPs and C-Corps and applying that knowledge to stock selection is critical. We maintain a highly concentrated portfolio focused on midstream companies with stronger balance sheets and lower leverage, advantaged geographic/asset footprint, cash flows supported by a more diversified customer base, and meaningful long-term volume contracts that can protect revenue streams. We have a bias for companies operating closer to the sources of demand and potentially less affected by commodity price swings, and we look for management teams that have demonstrated ability to successfully lead through energy cycles.

With the improving sentiment and fundamentals in natural gas, the current opportunity does not benefit every midstream company the same way, and we prefer select names with gathering operations in dry gas areas, such as the Marcellus and Haynesville basins, where activity is likely to pick up again in earnest.